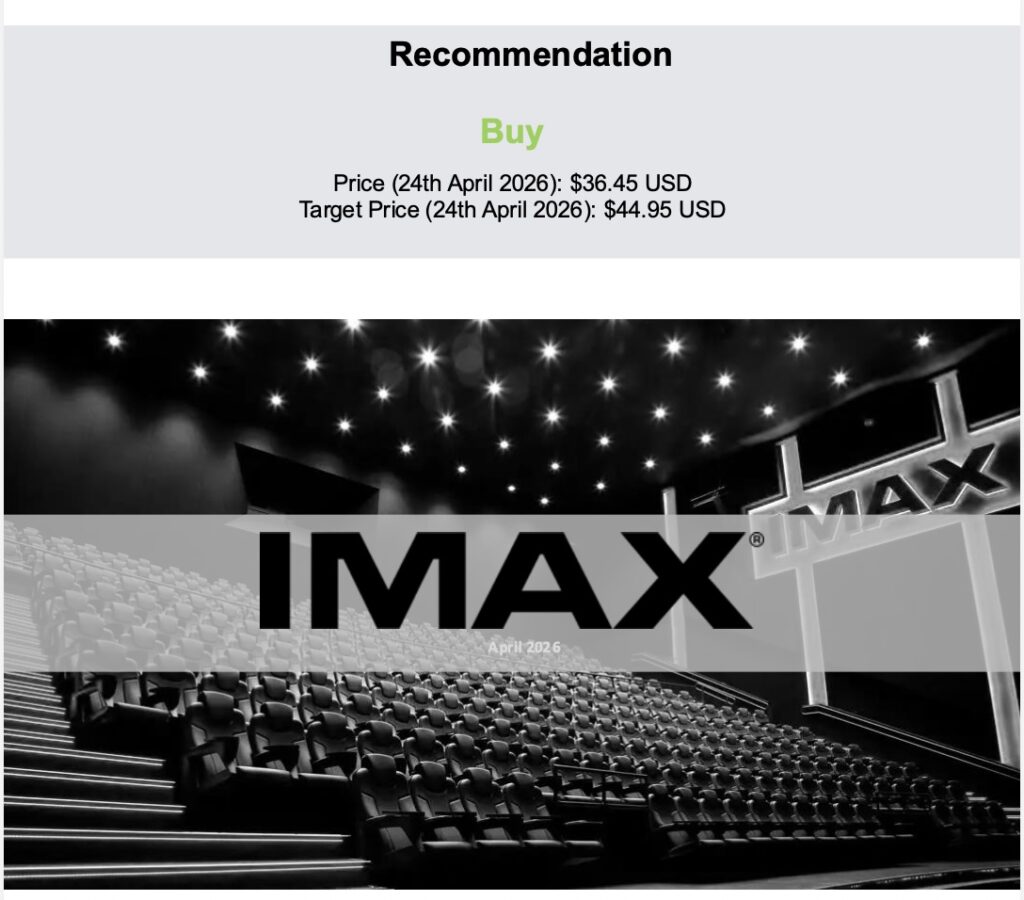

IMAX

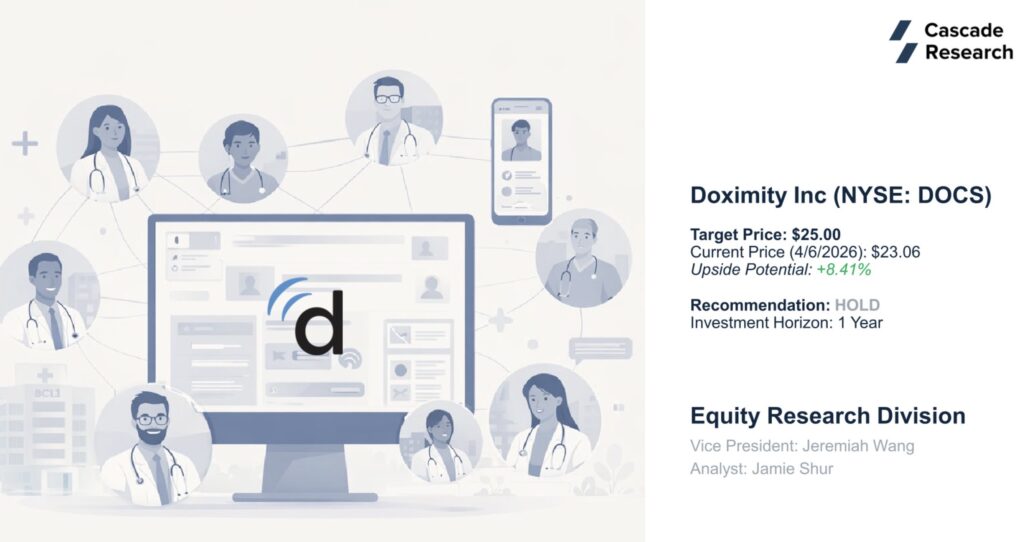

Doximity

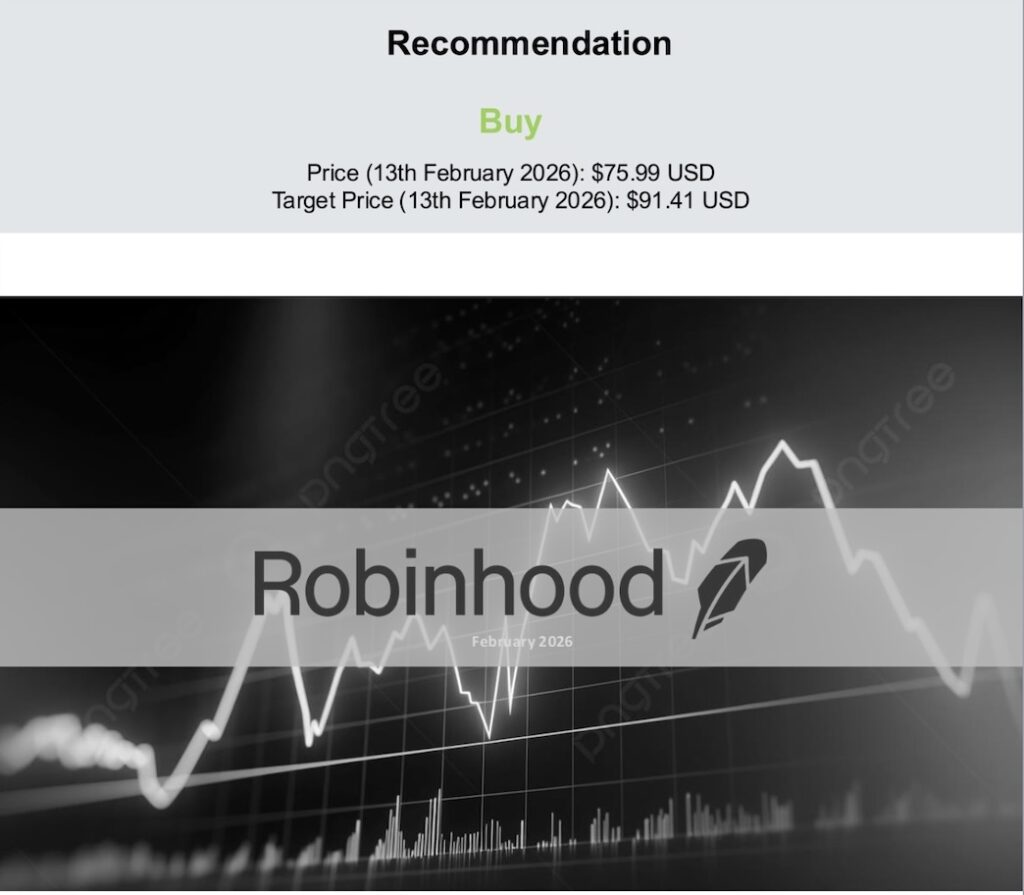

Robinhood

NextEra Energy

Snowflake

Iridium

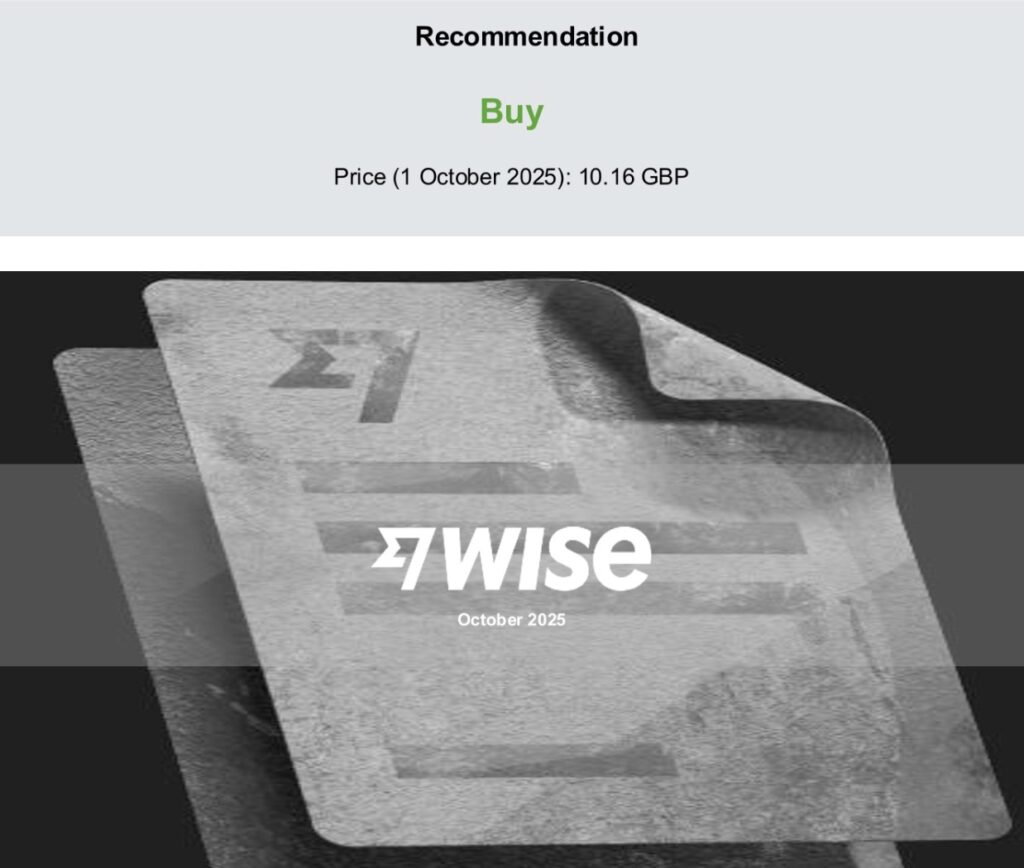

Wise